GOLD PRICE, US DOLLAR, STOCKS FORECAST

- The Fed’s decision on Wednesday could bring increased volatility for gold prices , the U.S. dollar and stocks

- The Federal Reserve is expected to hold its policy settings unchanged but could embrace a more dovish guidance

- Two possible FOMC outcomes are discussed in this article

The Federal Reserve will announce on Wednesday its first monetary policy decision of 2024. This event has the potential to create attractive trading opportunities, but it may also bring heightened volatility and unpredictable price movements, so traders should be prepared to navigate the complex market conditions later this week.

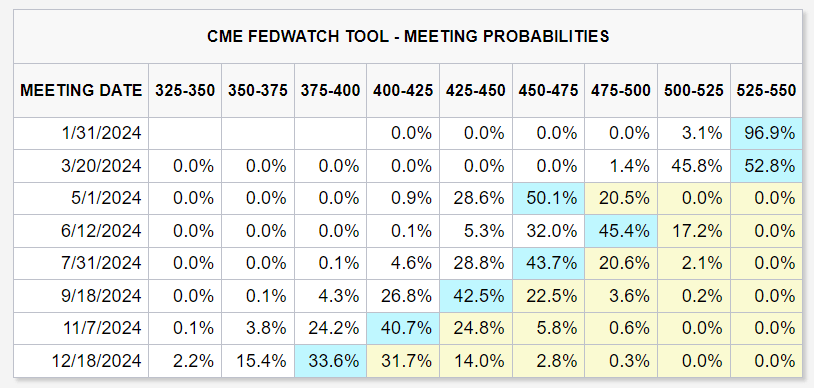

In terms of expectations, the FOMC is seen holding its key benchmark interest rate unchanged in its current range of 5.25% to 5.50%. The central bank may also drop language indicating a likelihood of additional policy firming from the post-meeting statement – a move that would mark a de facto shift toward an easing stance.

While the strong performance of the U.S. economy argues in favor of maintaining a tightening bias for the time being, policymakers may start embracing a more dovish posture for fear that that waiting too long to pivot may cause unnecessary damage to the labor market. In a sense, acting early minimizes the risk of having to implement more extreme accommodative measures later on when hell has already broken loose.

FOMC MEETING PROBABILITIES

Source: CME Group

It's still unclear whether the Fed will tee up the first-rate cut for the March meeting, but if it subtly greenlights that course of action, we could see a broad-based drop in U.S. Treasury yields, as traders try to front-run the upcoming move. This would be a bullish outcome for the stocks and gold prices , but would exert downward pressure on the U.S. dollar.

In the event of the FOMC leaning on the hawkish side and pushing back against expectations of deep rate cuts for the year and an early start to the easing cycle, nominal yields and the U.S. dollar should rise sharply in tandem. This scenario would create a hostile environment for the equity market as well as precious metals in the near term.